How Interactive Dynamics in Audit Workpaper Reviews Drive Quality and Growth

February 14, 2025

By Dr. Gabriel Saucedo, PhD, and Shruti Moolani, Chartered Accountant

The workpaper review process remains fundamental to both maintaining audit quality and guiding early-career auditors. Traditionally, audit review has relied on in-person discussions, allowing preparers and reviewers to clarify issues and exchange feedback in real-time. Yet, the rise of remote work, especially post-COVID-19, has introduced a new dependency on digital communication tools like email, Zoom, and firm-specific platforms. While these tools provide flexibility and convenience, they can also present challenges, sometimes resulting in misunderstandings or lacking the immediacy of face-to-face conversations that foster constructive feedback. This evolution has reshaped feedback dynamics within audit teams, offering both new opportunities and unique challenges. Recognizing the essential role of the review process in safeguarding audit quality, this article uncovers fresh insights and practical strategies for firms aiming to refine their approach. By blending the benefits of advanced technology with the unique advantages of in-person interactions, audit teams can enhance their review process, foster auditor development, and ultimately drive higher-quality outcomes.

An Overview of Research Across Big 4 and Beyond

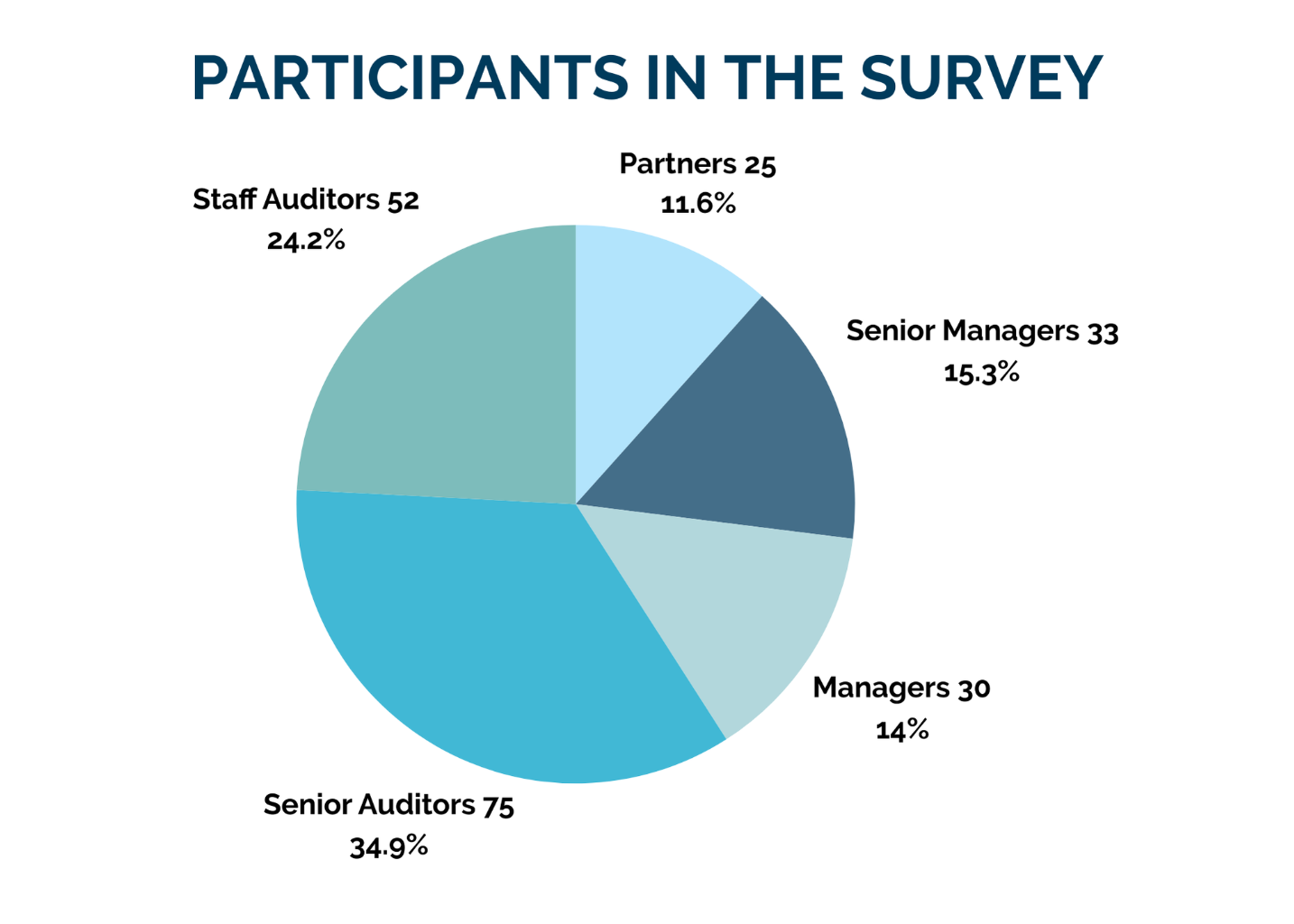

For this article, we build upon previously published academic works titled “Audit Roles and the Review Process: Workpaper Preparers’ and Reviewers’ Differing Perspectives”1 and “Shifting Styles: Do Auditor Performance Levels Influence the Review Process?,”2 both of which explore how distinct preparer and reviewer roles shape the review process. These studies use data surveyed from professionals across Big 4 and other prominent firms, examining how they are navigating changes in the review process. Survey responses from 215 participants (see table below) provide a balanced view, capturing experiences from professionals primarily working with public clients (65%) and others in non-public, governmental, and not-for-profit sectors.

Two parallel surveys were administered to collect data, one for preparers and another for reviewers. Partners and managers completed the reviewer survey, while audit staff participated in the preparer version, presenting a comprehensive look at how the review process is perceived from both vantage points. The data reflects a range of experience levels: reviewers, with an average of 11.3 years, bringing seasoned perspectives, while preparers, averaging 4 years, sharing task-focused insights.

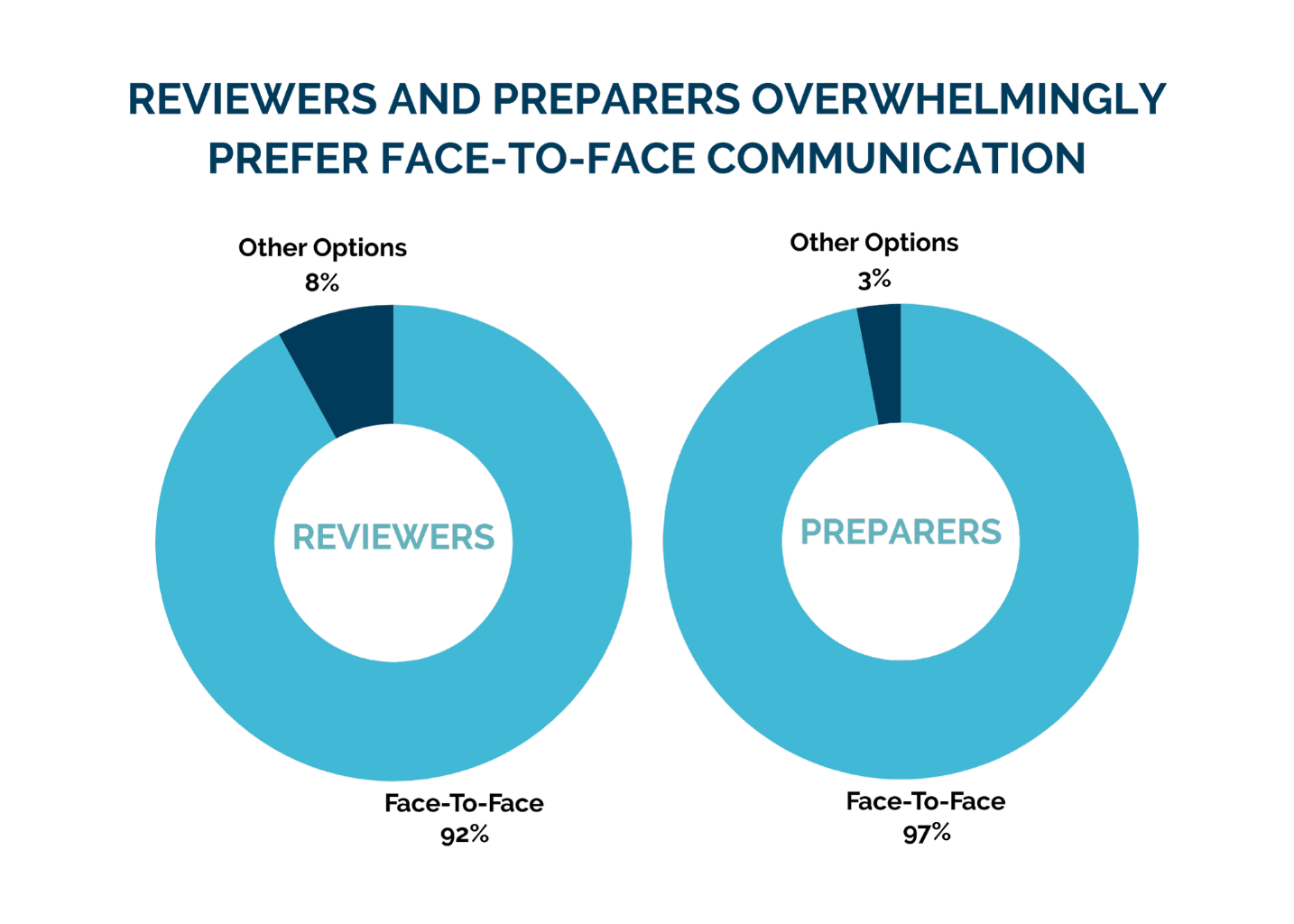

The referenced studies indicate that experienced auditors typically approach the review process by considering various factors, such as the preparer’s competency, audit complexity, and client-specific risks. Preparers, on the other hand, tend to focus on task-specific goals and often have a narrower view of the overall engagement. This divergence is expected, given that reviewers are responsible for the quality of the audit, while preparers concentrate on executing their tasks efficiently. Notably, both reviewers and preparers overwhelmingly preferred face-to-face communication for discussing review notes (92% of reviewers and 97% of preparers indicated this as their preferred method over telephone, e-mail, firm developed software, virtual [video conferencing] or other options). This may not be overly surprising, as in-person communication fosters clarity and prevents misunderstandings, which helps ensure feedback is conveyed accurately.

However, the increasing use of remote work has made face-to-face communication less frequent. Electronic tools, such as email, Zoom, and firm-developed platforms, are now more common. While convenient, many audit professionals worry that these tools can lead to misinterpretations and a lack of full understanding or comprehension, as they lack the immediacy of in-person discussions.

Another element of the aforementioned studies uncovers that auditors’ performance levels also significantly influence the review process. Higher-performing auditors tend to receive more empowering, strategic feedback, while lower-performing auditors receive more directive guidance. This reflects Situational Leadership Theory, where reviewers tailor their feedback based on the readiness and performance levels of preparers. Reviewers often provide broader, risk-focused feedback to senior preparers, while less-experienced auditors receive more specific procedural instructions.

Strengthening Team Collaboration in a Remote-First Audit World

Prioritizing In-Person Communication

With remote or hybrid work here to stay, there is unlikely a complete reversion to face-to-face work for all teams. However, wherever feasible, audit firms should prioritize face-to-face discussions for critical review notes, as these interactions allow for a more interactive exchange of ideas. Early career auditors, in particular, benefit from observing how review comments relate to broader audit risks. Firms could adopt a mixed approach, combining the flexibility of remote work with scheduled in-person interactions, such as periodic team meetings or client site visits. This not only enhances communication but also helps rebuild relationships within audit teams, which can be strained by remote work.

Enhancing Electronic Tools for Clearer Feedback

While face-to-face communication remains essential, audit firms must also adapt to the realities of remote work. Firms should invest in improving the usability of electronic review tools, ensuring that these platforms facilitate clearer, more interactive feedback. Current tools often lack the ability to engage reviewers and preparers in real-time discussions, leading to potential miscommunication. Collaboration platforms that integrate features like video conferencing or threaded discussions within workpapers could help simulate in-person interactions, allowing both parties to ask questions and clarify feedback in context. A two-tiered review process could also be beneficial, where initial review comments are provided electronically, followed by a video or in-person discussion to ensure the preparer understands the feedback.

Leveraging Remote Work for Professional Development

Remote work has provided preparers with new opportunities to observe client meetings and interactions between senior auditors and clients, allowing them to gain insights into the decision-making process. This visibility can aid in preparers’ professional development, offering learning experiences that were previously limited by travel budgets or office constraints. Firms should capitalize on this aspect of remote work by providing preparers with greater access to client discussions. This can help bridge the gap in professional development caused by reduced in-person interactions.

Innovative Strategies for Modernizing Audit Reviews

Customizing Training for Remote Communication

As remote work becomes the norm, effective digital communication is critical for maintaining audit quality. Custom training programs can help auditors develop skills for delivering clear and constructive feedback using electronic tools. A firm might implement a training module where auditors practice giving feedback in a simulated remote environment, using tools like Zoom and Teams, to ensure that their points are clear and actionable. This helps avoid common issues such as misinterpretation of feedback or delays in resolving review comments.

Emphasizing Mentorship and Shadowing

An early career auditor could be invited to virtually "shadow" a senior auditor during a critical client presentation or audit planning session, giving them real-time exposure to high-level discussions and decisions that enhance their learning experience. Even in a remote work environment, mentorship can be maintained through regular virtual check-ins and observation of key meetings.

Integrating Artificial Intelligence and Automation in Reviews

AI and automation tools can assist in the review process by flagging common errors, suggesting improvements, and reducing the workload for human reviewers. These tools can handle routine checks, allowing auditors to focus on more complex judgment-based tasks. For instance, A firm uses an AI-based tool to review financial documents, which automatically flags inconsistencies, freeing up auditors to focus on assessing overall audit risks and providing strategic feedback instead of spending time on manual checks.

Creating Feedback Portfolios for Auditors

A feedback portfolio is a compilation of all the review comments and suggestions an auditor receives over time, which can serve as a personalized development tool. For example, an early career auditor maintains a digital portfolio of feedback received over different audits. When preparing for a new audit, they review this portfolio to see recurring themes, such as the need to improve documentation, helping them proactively address weaknesses before the review process begins.

Conclusion

Overall, research highlights the critical role of effective communication in the audit review process, particularly the strong preference for face-to-face interactions among both reviewers and preparers. However, the increasing reliance on electronic communication tools, driven by technological advancements and remote work trends, poses challenges that must be addressed to maintain audit quality. To bridge the gap between traditional and modern communication methods, firms must enhance the effectiveness of electronic tools and provide training to ensure that review comments are clearly understood. By doing so, they can ensure that the benefits of technology do not overshadow the importance of personal interaction in the audit process.

What We’ve Learned About Audit Reviews: Insights from the Authors

Shruti Moolani: Throughout my career in audit and risk advisory, I have found the review process to be a critical component of my development as an auditor. Early on, face-to-face feedback was invaluable as it allowed me to quickly clarify issues and understand the bigger picture of audit risks, which sharpened my skills. As remote work became more prevalent, I noticed that while digital tools like email and Zoom offer flexibility, they sometimes lack the immediacy and depth of in-person discussions and a chance to connect more with my seniors and team. However, I’ve also seen the benefits of remote work, especially for early career auditors who can now observe senior auditors in client meetings, gaining insights they might not have had access to in traditional office settings.

Dr. Gabriel Saucedo: As I instruct my audit students each quarter (just as I did when I was a mentor and manager at KPMG), I emphatically communicate that review notes are arguably the best form of on-the-job training. Furthermore, students should be ready that firm leadership doesn’t hand out gold stars for every small task that is done correctly. However, review notes should not be viewed seen negatively. New accountants should view these review notes as areas for significant learning, growth, and improvement (although too many review notes may signal poor work performance).

Shruti Moolani holds a Chartered Accountant designation and is currently pursuing her Master’s in Accounting and Analytics (MSAA) at Seattle University. She previously worked at Wellness Forever Medicare Limited, BDO, and KPMG, all in India. smoolani@seattleu.edu

Dr. Gabriel Saucedo is an Associate Professor and Chair of the Accounting Department at Seattle University. Prior to completing his PhD at Virginia Tech, Gabriel earned his undergraduate business administration degree from Gonzaga University and worked at KPMG-Seattle in the audit practice. saucedog@seattleu.edu

This article appears in the winter 2025 issue of the Washington CPA magazine. Read more here.

- Ater, Brandon, et al. "Audit roles and the review process: workpaper preparers’ and reviewers’ differing perspectives." Managerial Auditing Journal 34.4 (2019): 438-461.

- Gimbar, C., Jenkins, J. G., Saucedo, G., & Wright, N. S. (2018). Shifting styles: Do auditor performance levels influence the review process? International Journal of Auditing, 22(3), 554-567.